Article by Michael Lebowitz from RIA Advice cross-posted via Zero Hedge.

A recent whitepaper by the Federal Reserve warns of “significantly lower profit growth and stock returns in the future.” In his article, End of an Era: The coming long-run slowdown in corporate profit growth and stock returns, Michael Smolyansky explains how the interest rate and corporate tax rate trends for the last thirty years provided a strong tailwind for corporate profits. As a result, stocks performed better than would have otherwise been the case.

Understanding why corporate profits and, ultimately, stock prices outperformed in the past is important. However, more critical for investors is the future and assessing how interest rates and tax rates will affect earnings growth and stock prices.

To expand on the article’s warning, we examine a few large well-known companies to see how lower interest and tax rates benefited their bottom lines. But first, we summarize the Fed article.

Key Takeaways

- GDP growth fell markedly over the last 30 years while corporate profit growth rose slightly.

- Lower interest and tax rates and increased leverage greatly benefited corporate net profits.

- McDonald’s, Pepsi, and Clorox support the Fed’s findings.

- Can profits maintain recent growth trajectories without the benefit of lower interest and tax rates?

End of an Era- Article Summary

The graph below shows that corporate earnings have grown faster over the last 30 years than in the 40 years before. The robust earnings growth occurred despite economic growth shrinking markedly.

Michael’s article attributes two key factors to explain the significant disconnect between the two growth rates. Per the article:

My central finding is that the 30-year period prior to the pandemic was exceptional. During these years, both interest rates and corporate tax rates declined substantially. This had the mechanical effect of significantly boosting corporate profit growth. Specifically, I find that the reduction in interest and corporate tax rates was responsible for over 40 percent of the growth in real corporate profits from 1989 to 2019.

Corporate profits would have grown by 4.50%, not 7.76% annually, without the boost from interest rates and taxes, assuming his 40% contribution calculation is correct. Such would be on par with GDP growth for the last thirty years. As we share later, it appears 40% is a reasonable estimate.

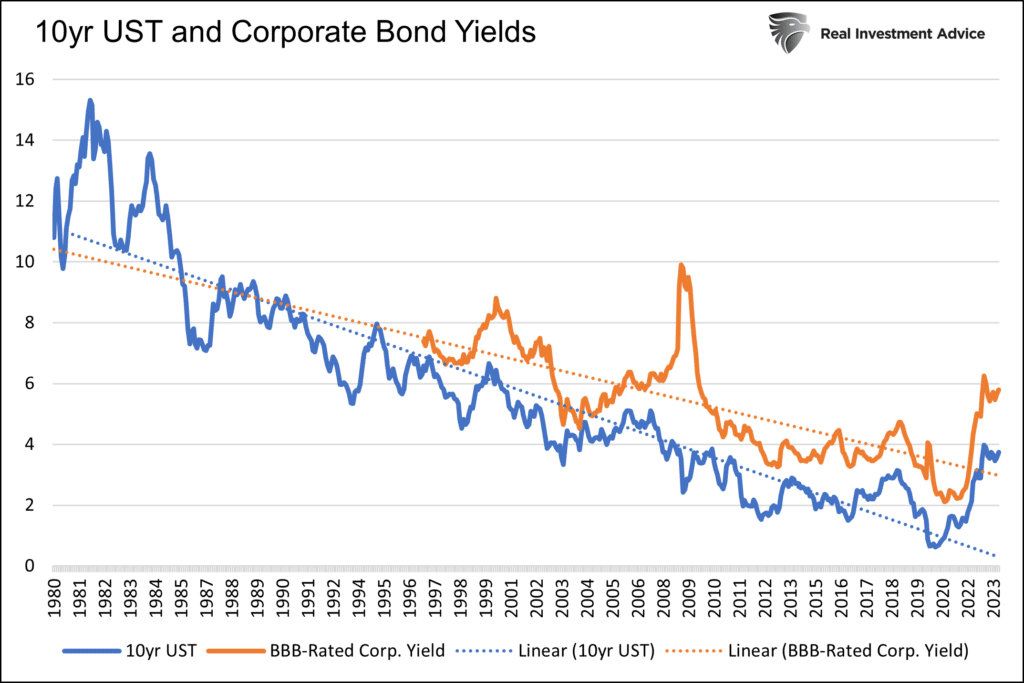

Interest Rates

As shown below, Treasury and corporate interest rates have fallen steadily over the last thirty years. As a result of cheap financing, corporate leverage, per the second graph below, has risen substantially to record highs. More leverage and reduced interest costs are a bona fide way to boost profits.

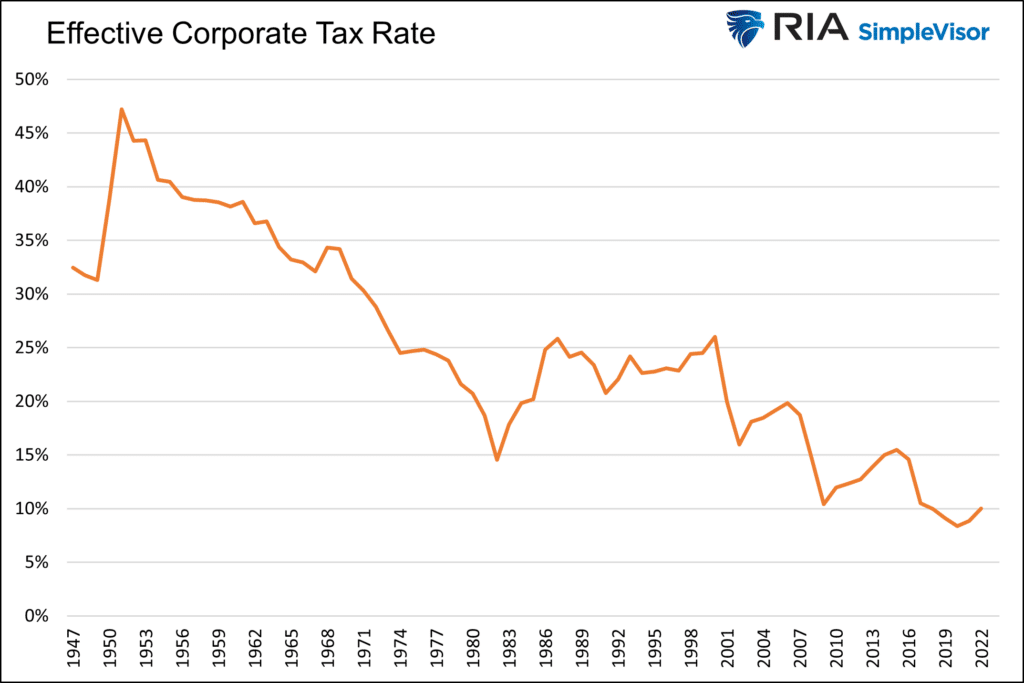

Tax Rates

Per the article:

By 1989, the effective corporate tax rate—measured as aggregate tax expenses divided by aggregate pre-tax income—stood at 34 percent, having fallen from an average of 44 percent over the period 1962 to 1982. From 1989 to 2007, ending just prior to the financial crisis, effective corporate tax rates averaged 32 percent. They then drifted somewhat lower in the years immediately following the financial crisis. The next major step down occurred following the passage of the Tax Cuts and Jobs Act of 2017, which cut the statutory corporate tax rate from 35 percent to 21 percent. With this reform, effective corporate tax rates fell from 23 percent in 2016 to 15 percent in 2019.

The graph below shows effective corporate tax receipts as a percentage of pre-tax income are now around 10% versus 25% in the late 1980s.

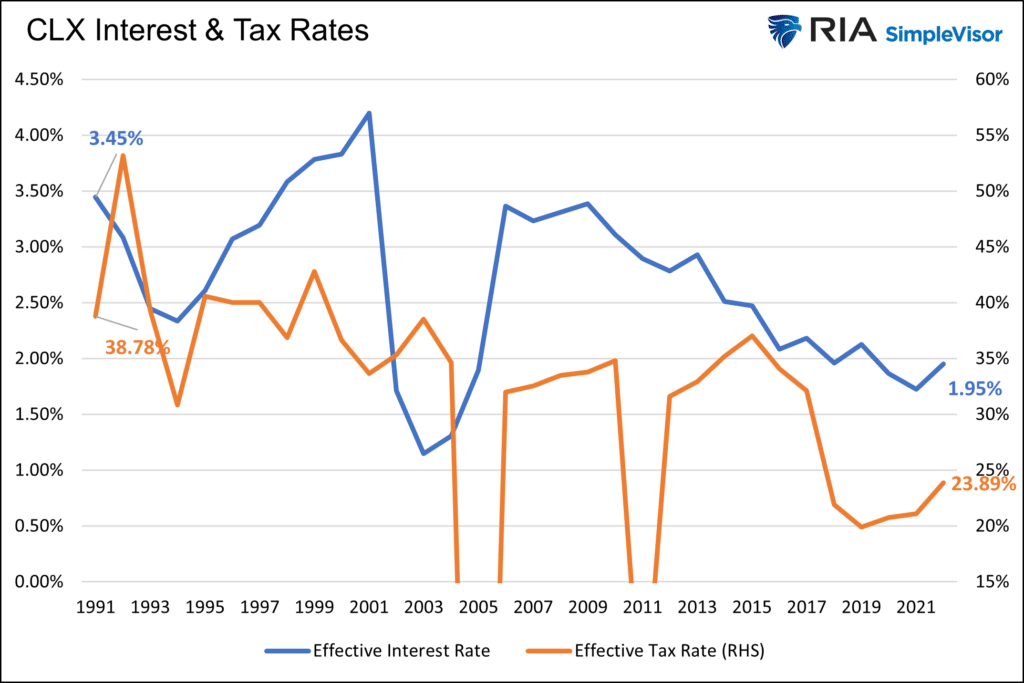

McDonald’s, Pepsi, and Clorox

To prove the benefit of lower interest and tax rates, we calculate how they helped improve profits for three large, well-known companies. The table below compares the debt levels, interest, and effective tax rates from 1990 to 2022 for McDonald’s, Pepsi, and Clorox.

Survival Beef on sale now. Freeze dried Ribeye, NY Strip, and Premium beef cubes. Promo code “jdr” at checkout for 25% off! Prepper All-Naturals

All three companies increased their debt load much more than their interest expenses due to lower rates. The effective interest rate decline was significant for McDonald’s and Pepsi. While not as dramatic, Clorox had a meaningful decline. Similarly, the effective tax rates for the companies fell between 15% and 20%.

Lower interest and tax rates had a meaningful impact on earnings, as shown at the bottom of the table. Michael Smolyansky’s estimate that interest and tax rates boosted earnings by about 40% in aggregate seems to be in the ballpark with our analysis. The graphs below the table show the change in interest and tax rates for the three companies over the last 30 years.

Future Interest and Tax Rates

While lower interest and tax rates boosted growth significantly, the ability for that to continue is negligible. The end of a rewarding era for stocks is likely behind us. Given that government deficits will continue to grow faster than the economy, it becomes increasingly unlikely that the government can afford to reduce corporate taxes. In fact, the odds favor raising taxes. Interest rates may fall back to the low levels of the last ten years. Still, unless rates go negative, there is little room on the margin for corporations to reduce their effective interest rate meaningfully.

Consequently, its likely corporate profit growth in aggregate will be closer to GDP growth rates in the future. The gap between GDP and profits we highlighted at the article’s opening will likely close. 4%’ish profit growth isn’t bad. But current high valuations are predicated on solid profit growth. GDP-like growth is not forecasted and will likely weigh on stock prices. Simply put, investors will not be willing to pay an above-average valuation for what will seem like below-average profit growth.

- Preserve your retirement with physical precious metals. Receive your free gold guide from Genesis Precious Metals to learn how.

Summary

Per the Fed’s End of an Era article:

It may be tempting to assume that the exceptional stock market performance over the last three decades will continue indefinitely. My analysis, however, indicates otherwise. Both stock returns and corporate profit growth are very likely to be substantially lower in the future. This conclusion follows from the minimal assumption that interest rates and effective corporate tax rates have very little scope to fall below 2019-levels.

The tailwinds of the last thirty years propelling profit growth by about 3% more than GDP are likely over. Without said help, profits are likely to track nominal GDP. However, we must remember that higher interest and tax rates are not out of the question. 4% profit growth may be the upside with a meaningful downside if interest rates stay around current levels and or tax rates increase.

As we wrote earlier:

Simply put, investors will not be willing to pay an above-average valuation for what will seem like below-average profit growth.

About the Author

Michael Lebowitz, CFA is an Investment Analyst and Portfolio Manager for RIA Advisors. specializing in macroeconomic research, valuations, asset allocation, and risk management. RIA Contributing Editor and Research Director. CFA is an Investment Analyst and Portfolio Manager; Co-founder of 720 Global Research.

Follow Michael on Twitter or go to 720global.com for more research and analysis. Customer Relationship Summary (Form CRS)

Five Things New “Preppers” Forget When Getting Ready for Bad Times Ahead

The preparedness community is growing faster than it has in decades. Even during peak times such as Y2K, the economic downturn of 2008, and Covid, the vast majority of Americans made sure they had plenty of toilet paper but didn’t really stockpile anything else.

Things have changed. There’s a growing anxiety in this presidential election year that has prompted more Americans to get prepared for crazy events in the future. Some of it is being driven by fearmongers, but there are valid concerns with the economy, food supply, pharmaceuticals, the energy grid, and mass rioting that have pushed average Americans into “prepper” mode.

There are degrees of preparedness. One does not have to be a full-blown “doomsday prepper” living off-grid in a secure Montana bunker in order to be ahead of the curve. In many ways, preparedness isn’t about being able to perfectly handle every conceivable situation. It’s about being less dependent on government for as long as possible. Those who have proper “preps” will not be waiting for FEMA to distribute emergency supplies to the desperate masses.

Below are five things people new to preparedness (and sometimes even those with experience) often forget as they get ready. All five are common sense notions that do not rely on doomsday in order to be useful. It may be nice to own a tank during the apocalypse but there’s not much you can do with it until things get really crazy. The recommendations below can have places in the lives of average Americans whether doomsday comes or not.

Note: The information provided by this publication or any related communications is for informational purposes only and should not be considered as financial advice. We do not provide personalized investment, financial, or legal advice.

Secured Wealth

Whether in the bank or held in a retirement account, most Americans feel that their life’s savings is relatively secure. At least they did until the last couple of years when de-banking, geopolitical turmoil, and the threat of Central Bank Digital Currencies reared their ugly heads.

It behooves Americans to diversify their holdings. If there’s a triggering event or series of events that cripple the financial systems or devalue the U.S. Dollar, wealth can evaporate quickly. To hedge against potential turmoil, many Americans are looking in two directions: Crypto and physical precious metals.

There are huge advantages to cryptocurrencies, but there are also inherent risks because “virtual” money can become challenging to spend. Add in the push by central banks and governments to regulate or even replace cryptocurrencies with their own versions they control and the risks amplify. There’s nothing wrong with cryptocurrencies today but things can change rapidly.

As for physical precious metals, many Americans pay cash to keep plenty on hand in their safe. Rolling over or transferring retirement accounts into self-directed IRAs is also a popular option, but there are caveats. It can often take weeks or even months to get the gold and silver shipped if the owner chooses to close their account. This is why Genesis Gold Group stands out. Their relationship with the depositories allows for rapid closure and shipping, often in less than 10 days from the time the account holder makes their move. This can come in handy if things appear to be heading south.

Lots of Potable Water

One of the biggest shocks that hit new preppers is understanding how much potable water they need in order to survive. Experts claim one gallon of water per person per day is necessary. Even the most conservative estimates put it at over half-a-gallon. That means that for a family of four, they’ll need around 120 gallons of water to survive for a month if the taps turn off and the stores empty out.

Being near a fresh water source, whether it’s a river, lake, or well, is a best practice among experienced preppers. It’s necessary to have a water filter as well, even if the taps are still working. Many refuse to drink tap water even when there is no emergency. Berkey was our previous favorite but they’re under attack from regulators so the Alexapure systems are solid replacements.

For those in the city or away from fresh water sources, storage is the best option. This can be challenging because proper water storage containers take up a lot of room and are difficult to move if the need arises. For “bug in” situations, having a larger container that stores hundreds or even thousands of gallons is better than stacking 1-5 gallon containers. Unfortunately, they won’t be easily transportable and they can cost a lot to install.

Water is critical. If chaos erupts and water infrastructure is compromised, having a large backup supply can be lifesaving.

Pharmaceuticals and Medical Supplies

There are multiple threats specific to the medical supply chain. With Chinese and Indian imports accounting for over 90% of pharmaceutical ingredients in the United States, deteriorating relations could make it impossible to get the medicines and antibiotics many of us need.

Stocking up many prescription medications can be hard. Doctors generally do not like to prescribe large batches of drugs even if they are shelf-stable for extended periods of time. It is a best practice to ask your doctor if they can prescribe a larger amount. Today, some are sympathetic to concerns about pharmacies running out or becoming inaccessible. Tell them your concerns. It’s worth a shot. The worst they can do is say no.

If your doctor is unwilling to help you stock up on medicines, then Jase Medical is a good alternative. Through telehealth, they can prescribe daily meds or antibiotics that are shipped to your door. As proponents of medical freedom, they empathize with those who want to have enough medical supplies on hand in case things go wrong.

Energy Sources

The vast majority of Americans are locked into the grid. This has proven to be a massive liability when the grid goes down. Unfortunately, there are no inexpensive remedies.

Those living off-grid had to either spend a lot of money or effort (or both) to get their alternative energy sources like solar set up. For those who do not want to go so far, it’s still a best practice to have backup power sources. Diesel generators and portable solar panels are the two most popular, and while they’re not inexpensive they are not out of reach of most Americans who are concerned about being without power for extended periods of time.

Natural gas is another necessity for many, but that’s far more challenging to replace. Having alternatives for heating and cooking that can be powered if gas and electric grids go down is important. Have a backup for items that require power such as manual can openers. If you’re stuck eating canned foods for a while and all you have is an electric opener, you’ll have problems.

Don’t Forget the Protein

When most think about “prepping,” they think about their food supply. More Americans are turning to gardening and homesteading as ways to produce their own food. Others are working with local farmers and ranchers to purchase directly from the sources. This is a good idea whether doomsday comes or not, but it’s particularly important if the food supply chain is broken.

Most grocery stores have about one to two weeks worth of food, as do most American households. Grocers rely heavily on truckers to receive their ongoing shipments. In a crisis, the current process can fail. It behooves Americans for multiple reasons to localize their food purchases as much as possible.

Long-term storage is another popular option. Canned foods, MREs, and freeze dried meals are selling out quickly even as prices rise. But one component that is conspicuously absent in shelf-stable food is high-quality protein. Most survival food companies offer low quality “protein buckets” or cans of meat, but they are often barely edible.

Prepper All-Naturals offers premium cuts of steak that have been cooked sous vide and freeze dried to give them a 25-year shelf life. They offer Ribeye, NY Strip, and Tenderloin among others.

Having buckets of beans and rice is a good start, but keeping a solid supply of high-quality protein isn’t just healthier. It can help a family maintain normalcy through crises.

Prepare Without Fear

With all the challenges we face as Americans today, it can be emotionally draining. Citizens are scared and there’s nothing irrational about their concerns. Being prepared and making lifestyle changes to secure necessities can go a long way toward overcoming the fears that plague us. We should hope and pray for the best but prepare for the worst. And if the worst does come, then knowing we did what we could to be ready for it will help us face those challenges with confidence.